Search

Search

Locations

Locations

BOCUSA 美国

BOCUSA 美国

Careers

Careers

Global Climate and Sustainability Disclosure Regulations: Recent Developments in China, EU, and US

Insights Strategy and Research DepartmentGlobal Climate and Sustainability Disclosure Regulations: Recent Developments in China, EU, and US

Regulations addressing climate- and environmental sustainability-related issues are becoming increasingly prevalent in the global regulatory landscape, including ESG disclosure requirements in China, Europe and the United States. The following highlight recent developments and are not exhaustive.

China

One of the major regulatory agencies of China that has issued rules on ESG is the China Securities Regulatory Commission (CSRC), which oversees the securities and futures markets of China, including the regulation of ESG disclosures for listed companies.

Most recently, in April 2024, the three major stock markets in China (Shenzhen, Shanghai, and Beijing), under the guidance of the CSRC, issued their respective trial guidelines, collectively named the Sustainability Report Guidelines, a mandate milestone as this is the first-ever disclosure requirements of its kind. Listed companies are required to disclose information on topics including but not limited to: environmental protection, energy consumption, emissions, social responsibilities, and governance structures.

European Union (EU)

In 2018, the European Union (EU) issued a transparency framework to improve corporate disclosures in the sustainable finance market with an emphasis on clarity and comparability, called the Sustainable Finance Disclosure Regulation (SFDR). In 2021, the legislation came into application.

The SFDR requires the people and organizations involved in buying and selling financial assets to disclose at the entity and product level how they integrate risks and impacts related to sustainability in their decision-making processes for investments. Additionally, the SFDR requires disclosures for financial products with claims of being sustainable.

The purpose of the regulation is to make the sustainability risks that can impact the value of investments clear to investors. Complementing this, the regulation is also meant to elucidate the effects investments have on the environment and society in reference to EU targets related to climate neutrality and sustainability.

Regarding comparability, another aim of the SFDR is to reinforce investor protection by increasing the ease by which investors can differentiate between the sustainability claims of financial products and services to therefore make better-informed investment decisions. In June 2024, the three European Supervisory Authorities published a joint opinion with insights gained from the functioning SFDR, calling for two product categories: sustainable and transition. Simplifying these categories with clear criteria supports a better understanding of the purpose of the products and reduction in greenwashing risks.

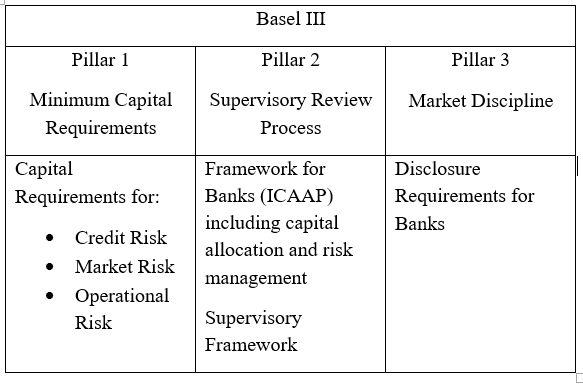

Basel III Pillar 3 Framework

Strengthening the regulation of banks, the Basel Accords are a set of international standards developed by a committee of banking supervisory authorities called the Basel Committee on Banking Supervision.

The third of the Basel Accords, called Basel III, is comprised of three pillars, the third of which addresses disclosure requirements for banks. Under Pillar 3, banks are required to disclose information related to ESG, including climate-related financial risks.

As part of the European Commission’s specific regulatory process for financial services, there are two types of technical standards: implementing and regulatory. In June 2024, the European Banking Authority (EBA) published updated implementing technical standards in alignment with the Basel III Pillar 3 disclosures.

The standards aim to ensure that stakeholders can make informed decisions with knowledge about the ESG risks and strategies of institutions, particularly through ratios that show how sustainability is being considered in risk management and business strategy.

The EBA framework is built on existing, widely adopted international initiatives and goes further with more granularly defined templates, tables, and instructions. Such requirements are meant to enhance the consistency, comparability, and meaningfulness of disclosures across institutions. In addition, through disclosures, institutions have an opportunity to promote awareness of their roles in the green economy and climate transition.

United States (US)

In March 2024, the United States federal government oversight agency called the Securities and Exchange Commission (SEC) adopted final rules on climate-related disclosures.

The SEC Climate Disclosure Rule requires companies that file with the SEC to provide climate change-related information in their filings, including registration statements and annual reports. Such information includes climate-related risks that impacted or are likely to impact the company’s business strategy, operations, or financial condition. Additional requirements include disclosures related to severe weather events and other natural conditions, climate-related targets and goals, internal carbon pricing, severe weather event reporting, and carbon offsets and renewable energy credits or certificates.

California

In late 2023, California passed two climate disclosure laws that require certain entities to report their greenhouse gas emissions and climate-related financial risks. They also require companies that make claims about achieving net zero emissions, carbon neutrality or greenhouse gas emissions reductions to disclose information supporting such claims.

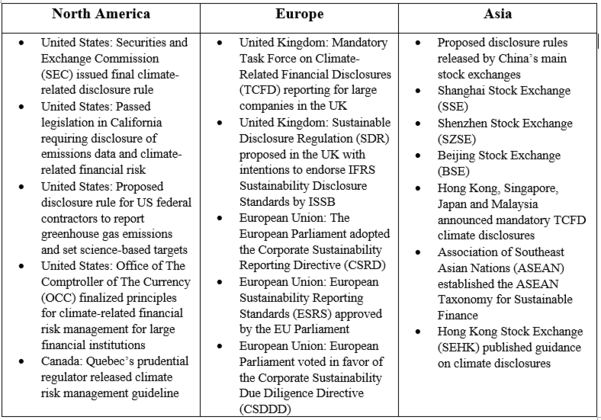

Global ESG Disclosure and Regulatory Landscape

Recent developments from government regulators in North America, Europe and Asia

The past few years saw a significant increase in ESG regulation globally. In most cases, implementation included a transition period for businesses to adopt new obligations. In 2024, further developments and enforcement are anticipated.

Adapted from Deloitte, Thomson Reuters, Bloomberg, The Conference Board.

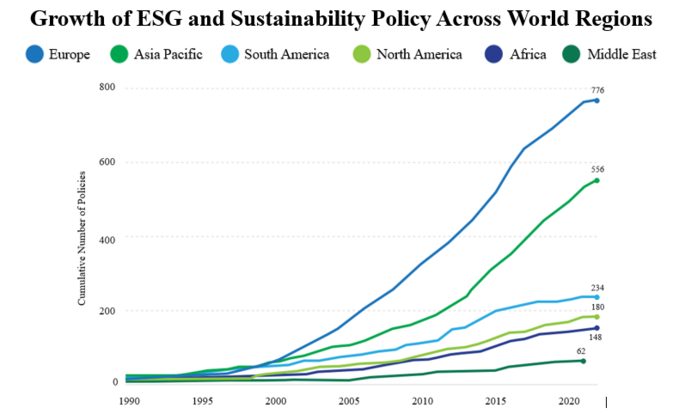

Based on a global database of mandatory and voluntary ESG policies, the most active policy issuers are located in Europe (776 policies, 31.5%), followed by Asia Pacific (556 policies, 22.5%). Countries in the Middle East (62 policies, 2.5%) and Africa (148 policies, 6%) are relative laggards. North America (180 policies, 7.3%) and South America (234 policies, 9.5%) show relatively slower policy growth trends. What is consistent across all world regions is the observation that ESG and sustainability policy growth is a relatively recent phenomenon of the last two decades.

Adapted from Carrots & Sticks Database.

Sources

1. https://www.responsible-investor.com/chinese-exchanges-endorse-double-materiality-in-market-first-disclosure-rules/

2. https://www.bloomberg.com/news/articles/2024-02-21/china-proposes-new-esg-rules-to-keep-up-with-european-guidelines

3. https://www.sustainablefitch.com/corporate-finance/chinas-new-disclosure-rules-to-boost-investor-confidence-in-esg-investments-23-02-2024

4. https://ballotpedia.org/Chinese_stock_exchanges_release_ESG_disclosure_guidelines_(2024)

5. https://corpgov.law.harvard.edu/2023/01/30/eu-finalizes-esg-reporting-rules-with-international-impacts/

6. https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en

7. https://corpgov.law.harvard.edu/2023/10/22/california-enacts-major-climate-related-disclosure-laws/

8. https://www.gtlaw.com/en/insights/2023/10/california-enacts-first-of-their-kind-laws-requiring-corporate-climate-disclosures

9. https://greenplaces.com/articles/california-sb-253-and-sb-261-explained/

10. https://www.carrotsandsticks.net/media/owwlefxh/2023-report-carrots-sticks.pdf

11. https://www.mwe.com/insights/californias-new-climate-disclosure-laws-what-you-need-to-know/

12. https://www.sse.com.cn/lawandrules/sselawsrules/stocks/mainipo/c/c_20240412_5737862.shtml

13. https://www.bse.cn/important_news/200021376.html

14. https://www.szse.cn/lawrules/rule/stock/supervision/currency/t20240412_606839.html